All Categories

Featured

Table of Contents

- – Is Level Term Life Insurance Vs Whole Life wor...

- – How can I secure Level Term Life Insurance Ben...

- – How do I get Level Premium Term Life Insurance?

- – Who offers flexible Level Term Life Insuranc...

- – What is the most popular Level Term Life Ins...

- – How long does Low Cost Level Term Life Insur...

The major distinctions between a term life insurance policy plan and a permanent insurance coverage (such as whole life or universal life insurance policy) are the duration of the policy, the build-up of a cash money worth, and the price. The ideal option for you will depend upon your needs. Below are some things to consider.

Individuals who possess entire life insurance policy pay a lot more in premiums for much less insurance coverage yet have the safety of understanding they are secured permanently. Level term life insurance policy. People that buy term life pay premiums for an extensive duration, yet they obtain nothing in return unless they have the tragedy to die before the term runs out

Also, considerable administrative costs often reduced right into the rate of return. This is the resource of the expression, "acquire term and spend the difference." The efficiency of permanent insurance policy can be consistent and it is tax-advantaged, offering additional advantages when the supply market is volatile. There is no one-size-fits-all solution to the term versus permanent insurance coverage argument.

The motorcyclist ensures the right to transform an in-force term policyor one ready to expireto an irreversible plan without undergoing underwriting or verifying insurability. The conversion cyclist must enable you to transform to any kind of irreversible plan the insurer provides without any constraints. The primary functions of the motorcyclist are keeping the original wellness score of the term policy upon conversion (also if you later have wellness problems or become uninsurable) and determining when and exactly how much of the protection to convert.

Is Level Term Life Insurance Vs Whole Life worth it?

Of program, overall premiums will raise dramatically given that whole life insurance is extra expensive than term life insurance policy - Level term life insurance for seniors. Clinical conditions that develop during the term life period can not create costs to be enhanced.

Whole life insurance policy comes with substantially greater monthly costs. It is suggested to offer coverage for as long as you live.

Insurance business established an optimum age limitation for term life insurance coverage policies. The costs also increases with age, so an individual aged 60 or 70 will pay significantly more than someone years younger.

Term life is rather comparable to auto insurance. It's statistically unlikely that you'll need it, and the costs are money away if you do not. If the worst happens, your household will receive the benefits.

How can I secure Level Term Life Insurance Benefits quickly?

___ Aon Insurance Services is the brand name for the brokerage and program management operations of Fondness Insurance coverage Solutions, Inc. (TX 13695) (AR 100106022); in CA & MN, AIS Affinity Insurance Policy Firm, Inc. (CA 0795465); in OK, AIS Affinity Insurance Solutions Inc.; in CA, Aon Fondness Insurance Services, Inc.

The Plan Representative of the AICPA Insurance Policy Depend On, Aon Insurance Coverage Solutions, is not associated with Prudential. Group Insurance coverage is released by The Prudential Insurance Firm of America, a Prudential Financial firm, Newark, NJ.

For the most component, there are 2 sorts of life insurance policy intends - either term or irreversible strategies or some combination of both. Life insurance firms provide numerous forms of term plans and conventional life plans in addition to "interest sensitive" items which have become a lot more common because the 1980's.

Term insurance coverage gives protection for a specific time period - Level term life insurance premiums. This period might be as short as one year or give coverage for a specific variety of years such as 5, 10, two decades or to a specified age such as 80 or in some cases up to the earliest age in the life insurance policy mortality

How do I get Level Premium Term Life Insurance?

Currently term insurance policy prices are really competitive and among the most affordable traditionally knowledgeable. It needs to be noted that it is an extensively held belief that term insurance is the least costly pure life insurance policy protection available. One needs to review the plan terms very carefully to choose which term life options are suitable to fulfill your certain scenarios.

With each brand-new term the costs is increased. The right to restore the plan without proof of insurability is an important benefit to you. Otherwise, the risk you take is that your wellness may deteriorate and you might be unable to obtain a policy at the same prices and even at all, leaving you and your recipients without insurance coverage.

You need to exercise this alternative during the conversion period. The size of the conversion duration will vary depending on the sort of term policy purchased. If you convert within the prescribed period, you are not called for to provide any information regarding your wellness. The costs rate you pay on conversion is generally based on your "existing acquired age", which is your age on the conversion date.

Who offers flexible Level Term Life Insurance For Seniors plans?

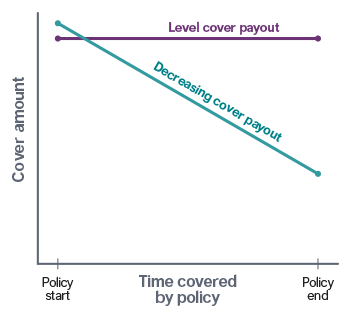

Under a degree term policy the face amount of the plan stays the same for the entire period. With decreasing term the face quantity reduces over the duration. The premium remains the very same each year. Frequently such policies are offered as mortgage defense with the amount of insurance coverage decreasing as the equilibrium of the home mortgage reduces.

Generally, insurance companies have not can alter premiums after the policy is offered. Because such policies might continue for years, insurance companies should use traditional mortality, rate of interest and expenditure price estimates in the costs computation. Adjustable premium insurance policy, however, enables insurance companies to offer insurance policy at lower "existing" costs based upon less conventional assumptions with the right to transform these costs in the future.

While term insurance is developed to provide security for a defined amount of time, permanent insurance coverage is made to provide coverage for your whole lifetime. To keep the costs rate level, the premium at the more youthful ages exceeds the real cost of defense. This additional premium builds a book (cash worth) which aids pay for the policy in later years as the expense of defense surges above the costs.

What is the most popular Level Term Life Insurance For Seniors plan in 2024?

With degree term insurance policy, the price of the insurance policy will remain the exact same (or possibly decrease if dividends are paid) over the regard to your plan, usually 10 or two decades. Unlike permanent life insurance policy, which never ends as lengthy as you pay costs, a degree term life insurance policy will certainly finish at some time in the future, typically at the end of the period of your degree term.

As a result of this, many individuals utilize irreversible insurance policy as a steady economic preparation tool that can offer numerous requirements. You may be able to transform some, or all, of your term insurance coverage throughout a collection period, generally the very first one decade of your policy, without requiring to re-qualify for insurance coverage also if your health has actually changed.

How long does Low Cost Level Term Life Insurance coverage last?

As it does, you might want to include to your insurance policy protection in the future. As this happens, you may desire to ultimately decrease your death advantage or consider transforming your term insurance coverage to a long-term plan.

Long as you pay your premiums, you can rest easy knowing that your loved ones will obtain a death benefit if you die throughout the term. Several term policies enable you the capability to convert to permanent insurance without needing to take an additional wellness test. This can enable you to make use of the added advantages of an irreversible plan.

{kind=link}

Table of Contents

- – Is Level Term Life Insurance Vs Whole Life wor...

- – How can I secure Level Term Life Insurance Ben...

- – How do I get Level Premium Term Life Insurance?

- – Who offers flexible Level Term Life Insuranc...

- – What is the most popular Level Term Life Ins...

- – How long does Low Cost Level Term Life Insur...

Latest Posts

Funeral Insurance For Under 50

Funeral Expense Insurance Plan

Funeral Insurance Quote

More

Latest Posts

Funeral Insurance For Under 50

Funeral Expense Insurance Plan

Funeral Insurance Quote